Lost In Translation: Key Deal Points In European vs. U.S. M&A Transactions – Corporate and Company Law

After two decades practicing law in Silicon Valley and five

formative years working on cross-border deals in Europe, I’ve

come to appreciate the subtle (and not-so-subtle) differences in

how merger and acquisition (M&A) transactions are structured on

either side of the Atlantic. For buyers and sellers on opposite

sides of the divide, these can be the difference between a smooth

closing and a deal that gets lost in translation.

Below, we look at the key distinctions between U.S. M&A deal

terms (sourced from SRS Acquiom) and European M&A deal terms

(sourced from CMS), personal insights from the trenches, and

practical takeaways for buyers and sellers trying to structure and

execute cross-border transactions.

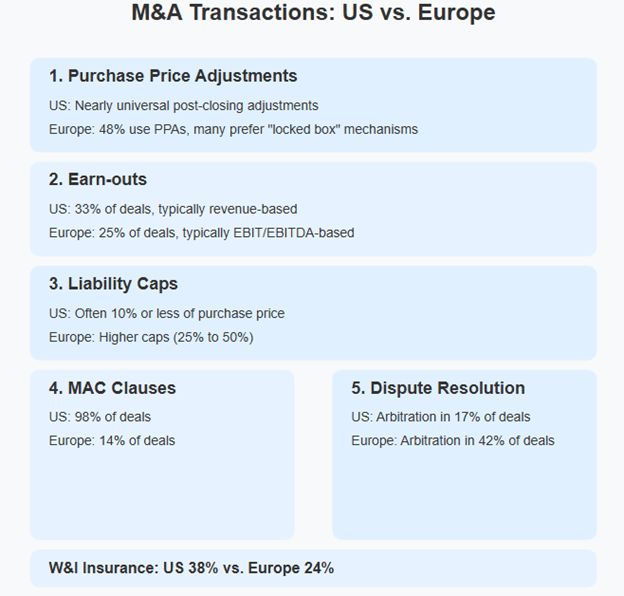

The infographic above provides a comprehensive overview of

the six key differences in M&A practices between the U.S. and

European markets. These points illustrate the fundamental

structural variations that deal teams must navigate when working

across borders.

1. Purchase Price Adjustments (PPA): Certainty vs.

Flexibility

In the U.S., PPAs are nearly universal. Buyers expect to be made

whole for gaps in working capital, shortfalls in cash in the bank,

and any remaining debt post-closing. It’s a well-oiled machine,

and most parties know the drill.

In Europe, it’s a different story. While PPAs are gaining

ground (found in less than half of all M&A deals per CMS), many

deals still rely on the “locked box” mechanism, where the

price is fixed based on a historical balance sheet, and the seller

warrants that there has been no leakage in value since the balance

sheet date. This approach offers price certainty but requires trust

and diligence.

U.S. clients doing deals in Europe should be open to lock box

structures, especially in competitive auctions. European clients

entering the U.S. should be ready for detailed post-closing

adjustments and the accounting gymnastics that come with them.

2. Earn-outs: A Tale of Two Metrics

Earn-outs are common in both markets, making up 33% of U.S.

deals and 25% of European ones. But the way they are structured

varies widely. In the U.S., revenue-based earn-outs are more

common, as opposed to Europe, where EBIT/EBITDA is king.

In tech and healthcare, where future performance is often

speculative, earn-outs can bridge valuation gaps. But they are also

a breeding ground for disputes.

Defining metrics clearly is table stakes, as is aligning

incentives and not underestimating the emotional toll of earn-out

negotiations, especially when founders are staying on board.

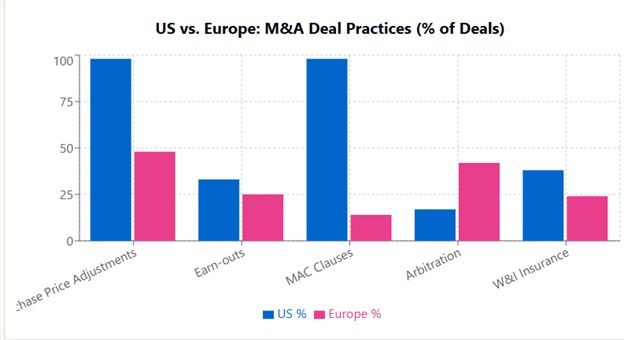

The chart above quantifies the prevalence of key M&A

practices in both markets. Note especially the dramatic difference

in MAC clause usage (98% in the U.S. versus just 14% in Europe) and

the inverse relationship in arbitration preference (17% U.S. versus

42% Europe). These statistical differences highlight the importance

of understanding regional norms when structuring cross-border

transactions.

3. Liability Caps: How Much Skin in the Game?

In the U.S., seller liability is often capped at 10% or less of

the purchase price, thanks to the widespread use of transactional,

or “rep and warranties” insurance (otherwise known as

“RWI”). In Europe, caps are higher, often 25% to 50%,

though RWI is catching up.

European sellers are more accustomed to bearing risk, while U.S.

sellers expect to shift it. This can lead to friction, so aligning

expectations early is key.

|

United States

|

Europe

|

|

|

Liability Cap Comparison

|

|

|

|

Legal Framework Differences

|

|

|

This interactive comparison illustrates the fundamental

differences in liability approaches and legal frameworks between

regions. Toggle between the tabs to explore how these differences

might impact deal structuring and negotiations. The higher

liability caps in Europe (25-50%) versus the U.S. (typically 10% or

less) reflect different risk allocation philosophies that must be

reconciled in cross-border transactions.

4. MAC Clauses: Rare in Europe, Routine in the U.S.

Material Adverse Change (MAC) clauses are standard in U.S. deals

and used in 98% of transactions. The idea is that between signing

and closing, the business has not suffered a MAC, and if it has,

the buyer does not have to close. Sometimes, it’s worded that

the business hasn’t suffered a MAC since the balance sheet

date. In Europe, however, they are rarefied air, appearing in only

14% of M&A deals, and often heavily qualified.

This can lead to surprises when U.S. buyers find no MAC clause

in a European deal, and European sellers may balk at the broad

language typical in U.S. agreements.

5. Dispute Resolution: Courts vs. Arbitration

Dispute resolution is where things really diverge. In the U.S.,

litigation is the default remedy, with arbitration used in only 17%

of deals. In Europe, the use of arbitration is much higher (42% of

deals in 2024), especially in cross-border transactions.

But there is a twist. 70% of European arbitration clauses apply

national rules, not international ones. That means a

“standard” arbitration clause in Germany may look very

different from one in France or the UK.

U.S. clients should be prepared for arbitration in Europe and

understand the local rules. European clients doing deals in the

U.S. should be ready for court proceedings and the discovery

process that comes with them.

6. Transactional Insurance: Growing, But Not Yet Global

RWI, or transactional insurance, is a game-changer. It smooths

negotiations, caps liability, and speeds up closings. In the U.S.,

it’s used in 38% of deals. In Europe, it’s at 24%, but

rising fast, especially in the UK and Germany.

I have seen RWI insurance unlock deals that would otherwise

stall over the scope of representations and warranties, indemnity

caps, or escrow mechanics. But it is not a silver bullet, so

underwriting diligence still matters.

Bridging the Gaps

Cross-border M&A is never just about the numbers. It’s

about culture, expectations, and communication. I have seen deals

that were super smart on paper fall apart because the

counterparties did not understand each other’s norms. And I

have seen unlikely partnerships thrive because they took the time

to bridge those gaps.

So, whether you’re a U.S. buyer eyeing a European AI

startup, or a European medtech platform bolting on a U.S. target,

remember that what is “market” depends on where you are.

When in doubt, ask someone who’s been on both sides of the

table.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link