RingCentral: Balanced Growth Strategy To Drive AI Sales And Generating Cash (NYSE:RNG)

")

LumiNola/E+ via Getty Images

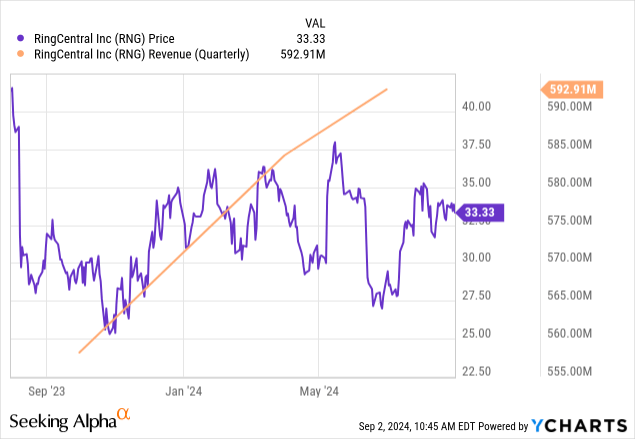

When I last covered RingCentral (NYSE:RNG) in July last year, I highlighted the advancements made in enhancing its product offerings using Generative AI and how this could improve sales. This has indeed been the case with revenues improving every quarter as shown below since then, but despite my bullish position, the stock dipped by around 19% and is trading around $33.33.

This thesis aims to show that this dip constitutes a buying opportunity as the stock is underpriced relative to the IT sector while it is generating above-average cash from operations thanks to its subscription model. I start by providing an update on how its AI-enhanced products have fared in the face of the competition as well as the strategy it has adopted to drive sales profitably together with related risks.

Transitioning to an AI-first company

First, RingCentral has a cloud-based communications-based platform that provides VoIP, video conferencing, and other messaging services including chat-based ones. This is referred to as CCaaS or Contact Center as a Service. Consequently, its line of business has been disrupted with the emergence of Gen AI and chat-based tools like ChatGPT, which the technology engenders.

In response, the company promptly integrated innovation into its product offerings since the middle of last year to gradually become an AI-first company, exemplified by its flagship RingCX, an intelligent contact center platform. Together with RingEX, the AI-integrated business phone system, the aim was to enhance customer interactions through better-informed agents, by providing them with real-time guidance and automating certain functions like monitoring and scoring.

www.ringcentral.com

Checking how these AI enhancements have translated into sales more than one year later, there has been good traction for RingCX which had over 350 customers at the end of the second quarter of 2024 (Q2), or a 70% increase on a sequential basis. Furthermore, together with RingEX, RingCX helped to drive the TCV (total contract value) of over $1 million by 25% which positively reverberated on the ARR per account. Thus, demand for AI-enhanced products contributed meaningfully to revenue growth in Q2.

Going forward, with the combined strength of the RingSense AI platform used for conversation intelligence which I will detail later, the company has set a goal of $100 million of ARR (Annual Recurring Revenue) from new products by the end of 2025.

Facing Competition and Disruption and the Growth Strategy

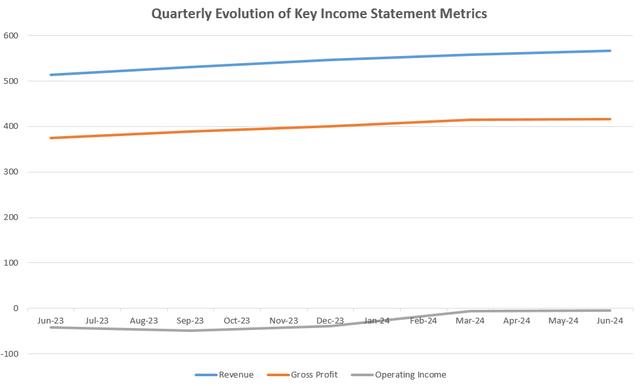

However, its transition to an AI-first CCaaS has not been accompanied by margin expansion, as operating income has remained negative as shown by the grey chart below, suggesting limited pricing power or deliberately keeping prices low to lure customers. Still, the operating losses have been controlled, resulting in operating income trending upwards from the March 2024 quarter. Noteworthily, losses were reduced to $4.2 million in Q2 compared to $38.5 million in the December 2023 quarter.

Table prepared using data from (www.seekingalpha.com)

Still, the challenge for RingCentral is to continue improving the cost structure while it scales as it faces competition from Zoom (ZM), Cisco’s (CSCO) WebEx, Microsoft Teams, 8×8 (EGHT), and Vonage which was acquired by Ericsson (ERIC) in 2022 for $6.2 billion. Also, as touched upon earlier, Gen AI is disrupting the CCaaS industry by providing new ways to promote the customer engagement process, which can encourage some companies to add interactive Chatbots to their websites instead of subscribing to a cloud contact center provider.

This begs the question of whether RingCentral will be able to deliver better profits while driving sales, especially since it has priced RingCX and RingSense together at $100 which may be on the low side considering that Gen AI can improve productivity by 30% to 45% according to McKinsey.

As a counterargument, RingCentral’s growth strategy seems to be based firstly on leveraging upselling opportunities to its existing client base, as opposed to scaling aggressively by spending relatively more marketing dollars to drive sales to new customers. Secondly, when it comes to customer acquisition, the aim appears to be more oriented toward selling to large organizations. Examples are the 5,000 RingEX and 500 RingCX seats sold to a county in the U.S. Mid-West, and the agreement with Vodafone (VOD) to resell RingCX to its worldwide user base. Looking further, there are collaborations with other GSPs (Global Service Providers), as these make the transition from on-premise to cloud communications while deepening customer engagements for UC (Unified Communications).

Third, there is product integration with ServiceNow (NOW), HubSpot, and Microsoft Teams, which eliminates the need for users to switch between applications, thereby reducing the time needed to resolve issues faced by the end customer. Noteworthily, there is the integration with Microsoft Teams, which also incorporates VoIP capabilities, making it a competitor. Therefore, RingCentral’s telephony features being available within Teams amounts to a strategic collaboration to enable users to make phone calls without leaving the collaboration tool.

Deserves Better because of Cash Generation, but Revenue Growth Could Slow

Thus, while the intent is clearly to grow and drive adoption for its innovation, RingCentral’s strategy appears more skewed towards balanced growth or one where the profitability aspect is also taken into consideration. Discussing further, while this strategy should not lead to a surge in sales, it will not boost operating income either as the company still has to spend money on R&D to constantly upgrade its offerings. Also, it incurred $434 million of expenses from share-based compensation in FY-23 alone.

On the other hand, the orange chart above shows its gross profits have evolved consistently with margins of around 70% for the last five quarters. This reflects the strength of its recurrent revenue model with the ARR from CCaaS increasing by 19% YoY to reach $390 million in Q2, helped by RingCX. This also reflects its ability to manage costs effectively by having an efficient platform.

Along the same lines, it boasts a high FCF margin of 24.68% which exceeds the IT sector median by 135%. This is in most part due to its subscription-based revenue model generated above-average cash flow from operations which have increased consistently during the last three years. Now, with the addition of AI enhancements on top of its existing offerings (instead of substituting one product for another), the steady and predictable stream of cash flow should continue.

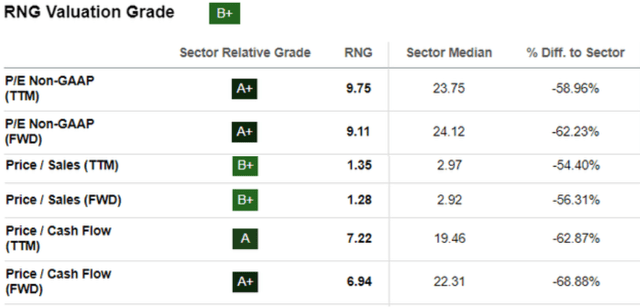

This means it deserves better since its forward price-to-cash flow is underpriced relative to the IT sector by 69% as pictured below. Considering a 20% upside, I have a target of $39.9 (33.33 x 1.2) based on the current share price of $33.33.

seekingalpha.com

This is about $5 less than the $45 estimated by analysts at Rosenblatt, but to justify my lower target, there is the balanced growth strategy used to drive product sales in light of the competition, and according to consensus analyst estimates, this should result in lower growth, in the range of 8.75% to 7.94% for FY-24 and FY-25 respectively. This means a deceleration relative to the 14% growth recorded in FY-25 and may not be well-digested by some growth-focused investors thereby putting some pressure on the stock. Future performance may be the reason why the stock has not performed better despite incrementing sales during the last five quarters, as per the blue chart above.

Still, I reiterate my bullish stance because of three factors, the first being the Federal Reserve potentially pivoting to a more dovish stance.

RingCentral is a Buy

In this respect, with only $200 million of cash in its balance sheet versus $1.59 billion of debt, the stock was severely impacted by the Fed aggressively raising rates as of March 2022 which means that logically the opposite should happen when the U.S. Central starts cutting rates later this month as more market participants are expecting. To this end, the debt load has also been reduced by more than $250 million from its December 2023 peak of $1.84 billion.

Second, the future revenue growth estimates of 8% to 9% could eventually be revised higher as they do not seem to capture the opportunities offered by RingSense for Sales, which is now used by over 800 customers with new bookings surging by three times on a sequential basis. The reason is this product has been augmented to include generative AI features like interactive search capabilities, and real-time note-taking, without forgetting conversation intelligence, which depending on the task at hand and the way it is applied can significantly improve collaboration across different communication channels.

Thus, it can be used to boost productivity for sales teams, especially when different mediums of communication like phone calls, SMS, and video meetings are being used given that it is integrated with certain CRM systems like Salesforce (CRM). Also, with its other AI products gaining traction, RingCentral could potentially continue growing at double digits given that the contact center market driven by Gen AI is expected to grow by a CAGR of 22.1% from 2024 to 2033.

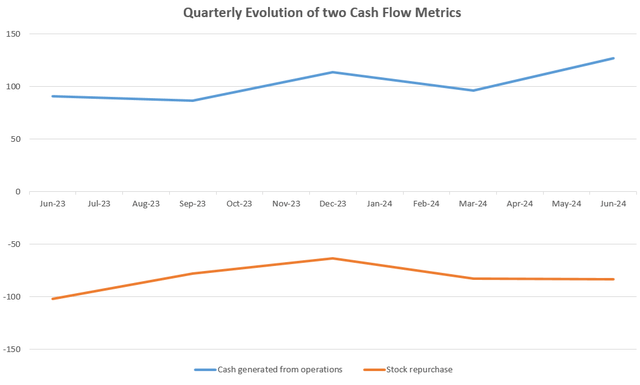

Third, to compensate for the large amount being spent on stock-based compensation (a non-cash expense) to make sure it attracts and retains the best talent in the highly competitive CCaaS industry, RingCentral has been repurchasing its stock as seen in the chart below, which also shows the cash generated from operations.

This not only returns value to shareholders as it acts as a lever to offset the dilution effect induced by stock-based compensation but also signals the management’s confidence in RingCentral’s long-term growth prospects.

Table prepared using data from (www.seekingalpha.com)

In conclusion, this thesis has shown that RingCentral is a buy with a 20% potential upside, but its balanced growth strategy may not boost sales as some may be expecting especially after delivering above 30% revenue growth in the 2021/2022 period in the aftermath of the COVID-19 pandemic, which accelerated the migration to cloud-based communications. Thus, the stock may suffer from volatility, but with the way, it is seeing traction with its AI-enhanced products, it is likely to exceed what analysts are expecting.

link