2024 Year In Review: Payday And Small-Dollar Lending – Corporate and Company Law

Welcome to the “Payday and Small-Dollar Lending”

chapter of our annual report, Consumer Financial Services: 2024 Year in

Review.

Looking Ahead to 2025

We expect the level of enforcement and regulatory activity in

the payday and short-term small-dollar loan space to decrease in

2025, at least at the federal level. The Consumer Financial

Protection Bureau (CFPB) was particularly active in this space

under the leadership of former Director Rohit Chopra, including

announcing interpretive rules and filing lawsuits related to

companies and industries that offer alternatives to traditional

payday and title loan products. Even if such scrutiny subsides, as

it did during the first Trump administration, we expect more

liberal-leaning states — such as California, New York, and

Massachusetts — to keep the payday and short-term

small-dollar loan industry in their crosshairs.

Key Trends From 2024

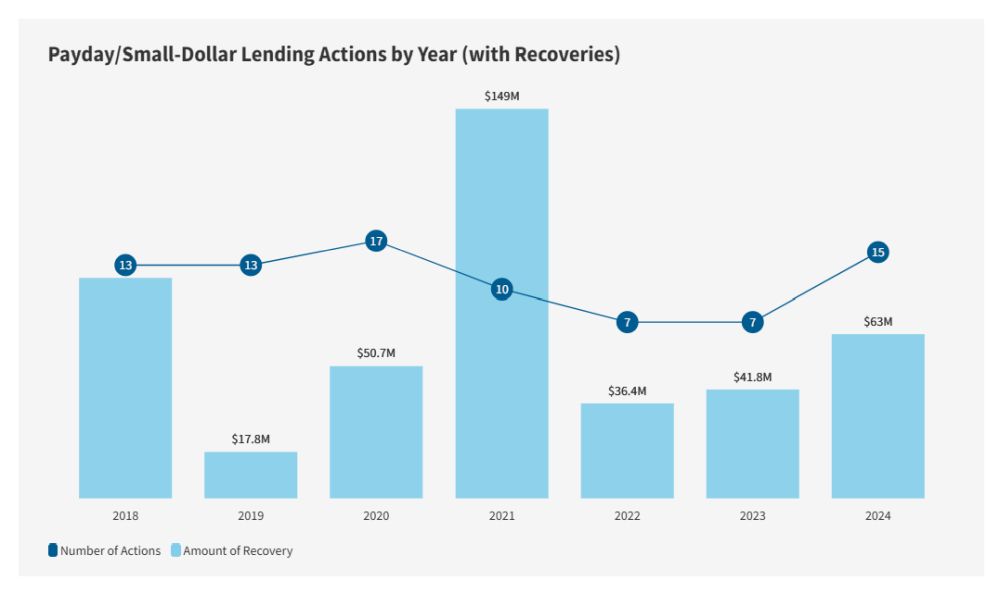

In 2024, Goodwin monitored 15 enforcement actions related to

payday or short-term small-dollar loans, an increase from the seven

such actions that Goodwin monitored in 2023. The total recoveries

in connection with such actions also increased year over year, from

$41.8 million in 2023 to $63 million in 2024.

In the News

CFPB Issues Interpretive Rule Identifying “Buy Now,

Pay Later” Lenders as “Card Issuers” Under

Regulation Z

In May, the CFPB issued an interpretive rule identifying

“Buy Now, Pay Later” (BNPL) lenders (i.e., lenders that

permit consumers to split purchases across multiple payments and

can require as little as a 25% down payment) as

“creditors” or “card issuers” for purposes of

Regulation Z, Subsection B. This requires such lenders to comply

with the consumer protection provisions set forth in Regulation Z.

The CFPB increased its focus on BNPL lenders beginning in 2021

after use of their products significantly increased. According to

the CFPB’s 2023 Making Ends Meet survey, 17% of consumers with

a credit record used BNPL for at least one purchase between

February 2021 and February 2022. Since 2021, the use of BNPL

products has only continued to increase, leading the bureau to

conclude that these products are essentially a digital replacement

for “conventional credit cards.” In response to this

interpretive rule, the Financial Technology Association (FTA) filed a

lawsuit against the CFPB in October, alleging, among other

things, that the CFPB exceeded its statutory authority. The CFPB answered the complaint in December 2024,

denying the FTA’s allegations. The case remains pending.

CFPB’s 2017 “Two Strikes and You’re

Out” Rule to Take Effect in March

In June, the CFPB announced that a regulation it

promulgated back in 2017 is now set to take effect in March 2025.

This “new protection” benefits payday loan borrowers. The

CFPB stated that the regulation, which adopts a rule known as the

“two strikes and you’re out” rule, was prompted by

the practice of lenders repeatedly attempting to withdraw money

from consumers’ accounts even when it was clear those accounts

were empty. The consumer would then be charged a fee for each such

failed attempt or, in some instances, the consumer’s account

would be closed. The “two strikes and you’re out”

rule prohibits lenders from trying more than twice to withdraw

money from a consumer’s account. If the two attempts are

unsuccessful, lenders would be permitted to make additional

attempts to withdraw only if the consumer specifically authorized

it. Due to lengthy litigation, the rule has yet to take effect.

That litigation, though, has since been resolved in the CFPB’s

favor, and the rule is now set to take effect in March 2025.

2024 Enforcement Highlights

FTC Reaches Settlement With Online Cash Advance

Provider

In January 2024, the Federal Trade Commission (FTC) announced its

settlement with an online cash advance

provider, FloatMe Corp., and its co-founders, resolving claims that the company violated the

FTC Act, Restore Online Shoppers’ Confidence Act, and Equal

Credit Opportunity Act (ECOA) by engaging in allegedly deceptive

marketing tactics and discriminatory practices. The FTC’s complaint alleged that the company

charged consumers a monthly membership fee and promised consumers

that they could instantly receive $50 cash advances but instead

allowed consumers to receive only $20 advances when they signed up

and charged extra fees for instant receipt of the cash advance. The

FTC also alleged that the company made it difficult for consumers

to cancel their subscriptions. This, the FTC alleged, resulted in

the cancellation process being “manual-only, delay-filled, and

error-ridden.” The FTC further alleged that FloatMe Corp.

discriminated against consumers who received public assistance such

as Social Security, military, and unemployment benefits by

declining advances to consumers whose income came from such public

assistance sources, despite still charging the consumers the

monthly fee. Under the settlement agreement, the company agreed to

pay $3 million to the FTC and to various injunctive relief,

including providing an easier method for cancellation and enacting

a fair lending program.

CFPB Sues Peer-to-Peer Emergency Credit Platform for

Alleged Violations of CFPA and FCRA

In May, the CFPB announced that it had filed a lawsuit against SoLo Funds Inc. in the

U.S. District Court for the Central District of California over

alleged violations of §§ 1031, 1036(a), 1054, and 1055 of

the Consumer Financial Protection Act (CFPA), 12 U.S.C.

§§ 5531, and 5536(a), 5564, 5565, and Section 607(b) of

the Fair Credit Reporting Act (FCRA), 15 U.S.C. § 1681e(b).

SoLo provides a platform through which consumers can request and

obtain emergency small-dollar short-term loans from other

consumers. The complaint alleges that SoLo promoted no-interest and

no-cost loans but that virtually all loans on the platform required

paying a “lender tip fee” and/or a “donation

fee.” The CFPB also claims that the company serviced and

collected on loans that were void and uncollectible under multiple

state laws because the loans were made and/or brokered by an

unlicensed individual or entity and/or the loans exceeded state

usury limitations. Because of this, the CFPB claims that the

company “deceptively, unfairly, and abusively represented that

these loan amounts were due and attempted to collect and collected

on those loans.” Furthermore, the CFPB alleges that the

company misrepresented that missed payments would be reported to

the credit bureaus as derogatory marks and would negatively affect

the consumer’s credit score when the company never reported

derogatory information to credit bureaus. The court denied

SoLo’s motion to dismiss the CFPB’s complaint, and the case

remains pending.

Massachusetts Attorney General Enters Into Assurance of

Discontinuance With California Finance Company

In May, the Massachusetts attorney general announced that

it entered into an Assurance of Discontinuance (AOD) with

EasyPay, a California-based financing company, resolving

allegations that the company had violated the Massachusetts

Consumer Protection Act. The attorney general alleged that the

company engaged in a “rent-a-bank” scheme, whereby the

company partnered with an out-of-state bank in an attempt to

circumvent Massachusetts’ maximum loan interest rates of 20%.

Although the out-of-state bank retained title to these loans, the

attorney general alleged that EasyPay is actually the “true

lender” of these loans because the company had a 90%

participation interest in the loans, took on the risk of

nonperformance on the loans, provided the marketing and customer

service for the loans, and provided the underwriting model for the

loans. The attorney general further alleged that, since 2018, the

average annual percentage rate of the loans was more than 100%. The

AOD provides that EasyPay will cease making, facilitating, or

servicing loans in Massachusetts and will cease collection on all

active and defaulted loans in Massachusetts. The company also

agreed to pay $625,000 in restitution to Massachusetts

consumers.

California Department of Financial Protection and

Innovation Revokes Company’s License for Failing to Provide

Information During Regulatory Exam

In July, the California Department of Financial Protection and

Innovation (DFPI) issued an order revoking the California

Financing Law license of Synapse Credit LLC, a company that had

offered both individual and business loans in the state, following

that company’s alleged failure to provide information during

the DFPI’s attempt to conduct a regulatory examination. In

June, the DFPI commenced a regulatory examination of the company

and requested copies of the company’s books, records, reports,

and other corporate data. According to the DFPI, the company

provided no documents, and the DFPI was thus unable to conduct the

regulatory examination and confirm that the company was complying

with California law.

CFPB and “Rent-to-Own” Company Exchange

Lawsuits in a Race to the Courthouse

In July, Acima Digital LLC and Acima Holdings LLC (together,

Acima) — a virtual “rent-to-own” company — sued the CFPB in the U.S. District Court for

the Eastern District of Texas, seeking declaratory and injunctive

relief. Days later, the CFPB announced the filing of a complaint against Acima in the

U.S. District Court for the District of Utah related to its

“virtual rent-to-own” products. The complaint alleges

that the defendants used “misleading” marketing and

“abusive” enrollment practices that target consumers with

poor or limited credit, locking them into costly

“financings” of household goods disguised as lease

transactions. The complaint further alleges that Acima reported

inaccurate information about such “financings” to

consumer reporting agencies and that these lending activities have

been connected to as many as five million consumer financing

agreements since 2015. According to the CFPB, this alleged conduct

violated the CFPA, the Electronic Fund Transfer Act (EFTA),

Regulation E, the Truth in Lending Act (TILA), Regulation Z, and

Regulation V. The CFPB further alleges that the company’s

former CEO provided substantial assistance to Acima in violating

the CFPA.

Court Dismisses CFPB Lawsuit Against Separate

“Rent-to-Own” Company; CFPB Then Files Amended

Complaint

In a separate litigation matter involving Snap Finance —

another “rent-to-own” company — the U.S. District

Court for the District of Utah granted Snap Finance’s motion to

dismiss the CFPB’s complaint, holding that Snap Finance’s

leases were not extensions of credit under the CFPA, TILA, or EFTA,

and, therefore, the CFPB lacked jurisdiction to bring a claim for

alleged violations of those laws. The dismissal was without

prejudice. The CFPB thereafter amended its complaint. Snap

Finance’s motion to dismiss the CFPB’s amended complaint

remains pending.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link