Anti-ESG Shareholder Proposals In 2025 – Executive Remuneration

Companies and investors use information related to

environmental, social or governance (“ESG”) factors to

provide a company-wide view of sustainability and other priorities.

This includes how the company discloses, reacts to and manages

ESG-related risks and policies, such as, for example, risks related

to carbon emissions, as well as policies addressing diversity,

shareholder rights and corporate social responsibility. These

topics are often the subject of shareholder proposals advocating

additional disclosure or policies in furtherance of ESG-related

goals. In contrast, “anti-ESG proposals” are generally

critical of, or question the value of, company policies or

initiatives related to these topics. As of the midpoint of the 2025

proxy season, “anti-ESG” proposals have become more

common, a trend mirroring that seen in recent years. In addition,

proponents that, in past proxy seasons, submitted proposals on

clearly anti-ESG topics, such as opposition to climate change-based

initiatives, are now submitting proposals on a broader array of

topics.

As of June 3, 2025, conservative proponents that traditionally

submitted anti-ESG proposals had submitted an aggregate of

approximately 120 shareholder proposals. This is approximately the

same number of proposals as were submitted by the same group of

proponents during the 2024 proxy season. Approximately 50 (45%) of

the 2025 proposals have been voted on to date and, notably, just as

in 2024, none of these proposals has received a majority

shareholder vote. About 15% have yet to be voted on, while the

remaining approximately 40% were not subject to a shareholder vote,

generally because they were withdrawn by the proponent or the

company was permitted to omit the proposal via the U.S. Securities

and Exchange Commission’s (the “SEC”) no-action

request process. Support levels for proposals ranged from a low of

0.20% to a high of almost 12%, with a median support level of 1.4%.

This is similar to the low of 0.03% support received in 2023;

however, proposals received as high as approximately 36% support in

2024. Notably, however, at the midpoint of the 2024 proxy season,

anti-ESG proposals had received a median support level of

approximately 1.5%, showing that support for these proposals

overall remains steadily low year over year.

No-Action Requests Related to Anti-ESG Proposals

Pursuant to Rule 14a-8 under the Securities Exchange Act of

1934, as amended (the “Exchange Act”), the SEC agrees

that it will not take action against companies that omit

shareholder proposals that meet certain criteria detailed in Rule

14a-8. To date, in the 2025 proxy season, companies submitted

approximately 55 no-action requests for proposals received from

proponents that typical submit anti-ESG proposals. This represents

a significant increase from the approximately 40 requests submitted

to the SEC staff (the “Staff”) during the 2024 proxy

season.

So far in 2025, the Staff has agreed that it would take no

action in connection with the omission of 30 such proposals, or

slightly more than half, an increase from the 40% of requests on

which the Staff agreed to take no action in 2024. In 2025, these

proposals spanned a wide-cross-section of issues, with multiple

proposals touching on traditional anti-ESG topics such as (i)

greenhouse gas (“GHG”) emissions, (ii) risks related to

religious discrimination, (iii) the use of diversity, equity and

inclusion (“DEI”) goals in setting executive compensation

and (iv) requests that companies consider abolishing their DEI

policies and goals. However, multiple proposals requested

assessments by a company’s board of directors “to

determine if adding Bitcoin to the company’s treasury is in the

best long-term interests of shareholders.” Bitcoin was the

subject of only one anti-ESG proponent shareholder proposal in

2024, which, since this topic is outside of those generally

considered to be anti-ESG, might show that proposal proponents are

expanding their interests.

The approximately 25 proposals that the Staff declined to omit

spanned a similar cross-section of issues, perhaps evidencing that

the Staff considers the unique facts and circumstances of each

company in determining whether to grant a no-action request. These

topics include requests that companies (i) consider abolishing DEI

programs and goals, (ii) revisit the use of DEI goals in setting

executive compensation, (iii) report on how their charitable

contributions “impact risks related to discrimination against

individuals based on their speech or religious exercise” and

(iv) report on oversight of “risks related to discrimination

against ad buyers and sellers based on their political or religious

status or views.” Interestingly, almost all of these proposals

were confined to traditional anti-ESG topics, with a strong leaning

toward proposals related to potential discrimination regarding free

speech and/or religious exercise. The proposals that have been

voted on received favorable votes ranging from 0.20% to almost 9%;

however, all but one proposal received support of approximately 2%

or less.

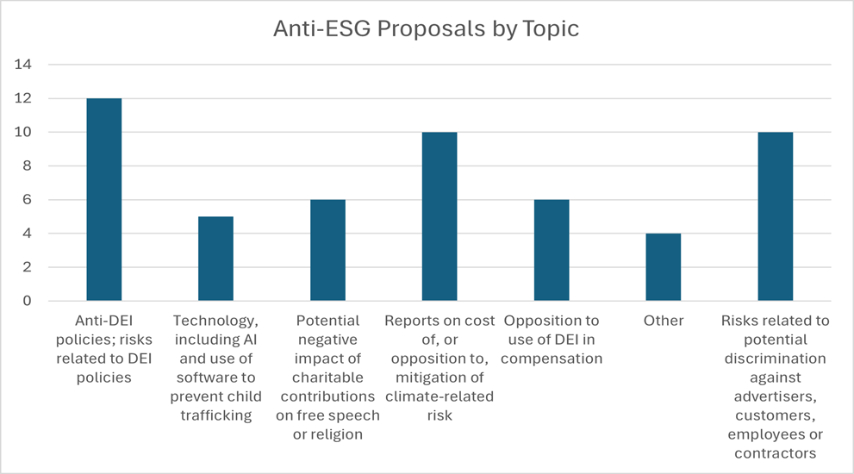

Topics and Trends in Anti-ESG Proposals

A majority of the anti-ESG proposals voted on so far in 2025

deal with topics thought to be traditionally anti-ESG, such as

challenging DEI programs or opposing efforts to mitigate climate

change. The proposals can be categorized as follows:

The proposals can be further cataloged as follows:

Anti-DEI Proposals

Collectively, proposals touching on DEI, such as (i) opposing

the use of DEI in setting executive compensation, (ii) requesting

that companies consider abolishing DEI policies or (iii) asking for

reports on the risks of such policies, constitute more than 40% of

the anti-ESG proposals voted on to date in 2025. These proposals

received a maximum of around 3% of shareholder support. Anti-DEI

proposals were less common in 2024, with only two proposals

opposing the use of DEI in executive compensation, and an

additional approximately 10 proposals asking for reporting topics

such as the “potential risks associated with omitting

“viewpoint” and “ideology” from its written

equal employment opportunity policy” or the “impacts of

DEI policies on civil rights, non-discrimination and return to

merit, and the impacts of those issues on the Company’s

business.” Anti-DEI proposals in 2025 tended to be more

strongly worded, including clear requests that companies consider

abolishing DEI policies altogether, perhaps reflecting the current

political climate in the United States. In both years, to date, all

proposals received low levels of shareholder support.

Proposals Regarding Free Speech and Religious

Exercise

A large number of anti-ESG proposals in both 2024 and 2025

focused on the views expressed and the policy positions taken by

companies, officers and directors, and the potential impact of such

views and actions on the company’s financial condition.

Proposals seemed to focus on two main areas: risk of negative

impacts of certain charitable giving and risks of discrimination

via policy or action.

Charitable Giving

In both 2024 and 2025, a number of anti-ESG proposals centered

on charitable giving. In 2025 to date, approximately five companies

received a proposal requesting an analysis of how a company’s

“contributions impact its risks related to discrimination

against individuals based on their speech or religious

exercise.” In addition, a very small number of proponents

requested the creation of a board committee to oversee and/or a

report on the impact of a company’s policies and/or charitable

giving on its financial sustainability, generally alleging that

companies contribute to organizations that “attack free speech

and religious freedoms.” However, in 2024, approximately 12

companies received an almost identical proposal to the latter,

supported, at least in some cases, by the statement that

“company bottom-lines, and therefore value to shareholders,

drop when companies take overtly political and divisive positions

that alienate consumers.” Taken together, this may demonstrate

that investors’ interest in charitable giving continues to

evolve. In 2024 and to date in 2025, these proposals all received

low levels of shareholder support.

Risks of Discrimination via Policy or Action

In 2025 to date, approximately 20% of the proposals voted on to

date dealt with risks related to discrimination based on the

exercise of free speech or religion. Slightly less than 10

proposals asked for reports on how a company “oversees risks

related to discrimination against ad buyers and sellers based on

their political or religious status or views,” alleging

censorship “for expressing disfavored political and religious

viewpoints.” Additionally, a small number of proposals

requested a report on risks related to religious or other

discrimination against employees, or discrimination against

customers.

In 2024, proposals related to discrimination also constituted

around 20% of the anti-ESG proposals subject to a shareholder vote.

However, almost all of the 2024 proposals specifically asked for

companies to issue reports on risks related to discrimination

against individuals, customers and/or employees based on factors

including religion, and/or whether this may impact individuals’

exercise of their civil rights or the company’s business. The

2025 proposals, detailed above, were more varied and used stronger

language, including references to “censorship” of certain

views. As yet, none of these proposals in either year have received

more than approximately 2% shareholder support.

Proposals Relating to Climate-Based Risk

In 2025 to date, almost 20% of anti-ESG proposals opposed

company responses to climate-based risks, such as requests for

reports on costs, benefits and/or risks arising from voluntary

environmental activities, such as carbon-reduction commitments, or

requests to remove all GHG emissions reduction targets. The

overwhelming majority of these proposals that have been voted on

received less than 3% shareholder support.

In 2024, an almost equivalent percentage of anti-ESG proposals

on which shareholders voted were related to climate-based risk,

showing ongoing interest in this topic, perhaps especially in light

of the SEC’s adoption of rules regarding the disclosure of

climate-based risk.1 However, the rules became subject

to litigation almost immediately after adoption, and on February

11, 2025, then Acting SEC Chair Mark Uyeda publicly stated his

request that the Eighth Circuit Court of Appeals postpone arguments

in the case.2 Subsequently, on March 27, 2025, the SEC

voted to end its defense of the rules, such that it is difficult to

predict whether the number of shareholder proposals focused on

climate-based risk will remain constant in 2026.3

Importantly, all but one of the 2024 proposals received

approximately 3% support or less, in line with overall low support

in 2025.

Proposals About Technology and Artificial

Intelligence

In terms of technology-focused proposals, even anti-ESG

proposals are not immune to the growing focus on artificial

intelligence (“AI”). The same proposal, requesting a

report assessing the risks posed to each company and the public due

to the real or potential improper use of data in developing,

training, and deploying AI offerings, as well as the steps taken to

mitigate these risks, received high levels of shareholder support

at several different companies, averaging around 10%. In 2024,

anti-ESG proponents submitted a single identical proposal,

receiving approximately 35% support, the highest of any anti-ESG

proponent proposal that year. We will have to wait to see if the

increasing frequency of AI-focused proposals, outside of the topics

generally addressed by conservative proponents, continues in future

years, but it seems clear from the relatively large shareholder

support on which companies and investors will continue to

focus.

Corporate Governance Proposals

In 2024, a small number of anti-ESG proponents submitted

proposals related to corporate governance topics. Examples include

a prohibition against directors simultaneously sitting on the

boards of two or more other companies and two or more non-corporate

organizations, and proposals mandating a separate chair of the

board and chief executive officer. However, we did not find a

significant number of corporate governance-related proposals from

anti-ESG proponents in 2025, so it will be interesting to see what

happens in 2026.

Key Takeaways

So far, the 2025 proxy season has demonstrated that, in spite of

a seeming increase in public anti-ESG sentiment and anti-ESG

shareholder proposals, support for anti-ESG measures remains low.

Notwithstanding, anti-ESG proponents appear to be broadening their

agendas—from familiar attacks on DEI initiatives and

climate-related targets to newer demands addressing political or

religious discrimination, cryptocurrency treasury strategies,

artificial intelligence oversight and, to a lesser extent,

traditional governance reforms—thereby compelling issuers to

respond to an ever-wider array of proposals. Companies were more

aggressive in seeking SEC no-action relief this year, and, overall,

the Staff was more willing to grant it. However, roughly half of

challenged proposals nevertheless survived.

The guidance in SLB 14M seems to have made it slightly easier

for companies to exclude shareholder proposals that do not directly

tie a significant policy issue to the company’s business;

however, the Staff’s decision-making regarding no-action

requests remains somewhat opaque. In light of this, boards and

management teams should continue to refine their

shareholder-engagement protocols, maintain clear rationales for

ESG-related policies, and ensure that disclosure controls are

calibrated to address both pro- and anti-ESG scrutiny, recognizing

that while anti-ESG activism shows little sign of swaying the

broader investor base, it will persist as a vocal and procedurally

sophisticated force in the proxy landscape.

Footnotes

1 See back)

2 See back)

3 See back)

Originally published by Harvard Law School Forum on Corporate

Governance

Visit us at mayerbrown.com

Mayer Brown is a global services provider comprising

associated legal practices that are separate entities, including

Mayer Brown LLP (Illinois, USA), Mayer Brown International LLP

(England & Wales), Mayer Brown (a Hong Kong partnership) and

Tauil & Chequer Advogados (a Brazilian law partnership) and

non-legal service providers, which provide consultancy services

(collectively, the “Mayer Brown Practices”). The Mayer

Brown Practices are established in various jurisdictions and may be

a legal person or a partnership. PK Wong & Nair LLC

(“PKWN”) is the constituent Singapore law practice of our

licensed joint law venture in Singapore, Mayer Brown PK Wong &

Nair Pte. Ltd. Details of the individual Mayer Brown Practices and

PKWN can be found in the Legal Notices section of our website.

“Mayer Brown” and the Mayer Brown logo are the trademarks

of Mayer Brown.

© Copyright 2025. The Mayer Brown Practices. All rights

reserved.

This Mayer Brown article provides information and

comments on legal issues and developments of interest. The

foregoing is not a comprehensive treatment of the subject matter

covered and is not intended to provide legal advice. Readers should

seek specific legal advice before taking any action with respect to

the matters discussed herein.

link