Dealmaker’s Digest: A Top 10 Bulletin – January 2025 – Corporate and Company Law

In Dealmaker’s Digest, read the top 10 latest developments

in global transactions. We offer insights into M&A activity

across industries and borders. To receive our M&A thought

leadership, please join our mailing list.

Key Takeaways

- Annual global M&A activity in 2024

rebounded significantly from 2023’s sluggish deal landscape.

Aggregate value of transactions ($100m+) increased 14% across all

buyer types, with sponsor-led deals jumping 36%

year-over-year. - Crossborder transactions played a key role for

dealmakers in 2024. Inbound U.S. transactions, totaling nearly

$350B, jumped 21% from 2023, while outbound U.S. activity rose 18%

(surpassing $430B for the year). - More mega-deals were struck in 2024 compared

with 2023; more than 25 U.S. transactions exceeded $10B in value, a

23% increase.

Global M&A Activity Update

1. Deal Value Trends

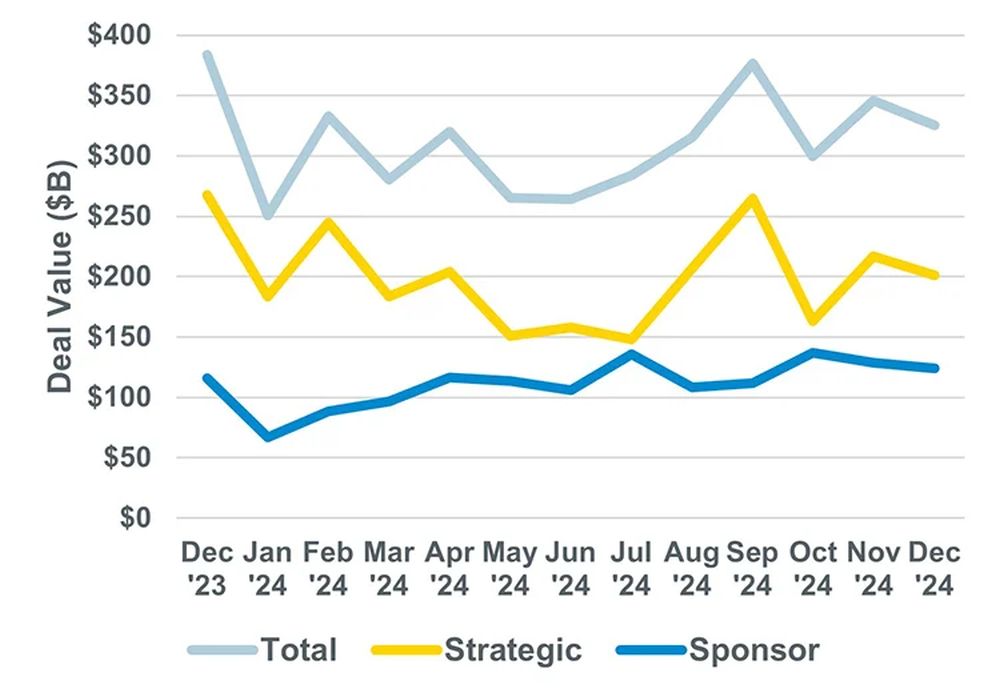

![]() Aggregate global monthly deal

Aggregate global monthly deal

value1 decreased moderately in December, down about $20

billion (6%) from November. Total monthly deal value decreased 15%

year-over-year.

![]() Transactions involving strategic

Transactions involving strategic

buyers in December also declined in value (7%) from November.

Strategic deal value in December dropped 25% year-over-year.

![]() Financial, or sponsor, buyer

Financial, or sponsor, buyer

transactions in December held steady, decreasing only 4% from

November, rounding out a comparably steady Q4 for sponsor

acquisitions. Sponsor buyer deal value increased 7%

year-over-year.

2. Deal Count Trends

![]() Global deal count held steady

Global deal count held steady

from November to December, ticking up 4%, and rounded out the most

active quarter by count for the year. Monthly deal count increased

16% year-over-year.

![]() Strategic buyer deal count in

Strategic buyer deal count in

December increased moderately, up 6% from November and 11%

year-over-year.

![]() Sponsor buyer deal count in

Sponsor buyer deal count in

December remained steady month-over-month, decreasing just 1% from

November. However, sponsor deal count rose dramatically (28%)

year-over-year.

3. Annual Global M&A Activity (Transactions

$100M+)

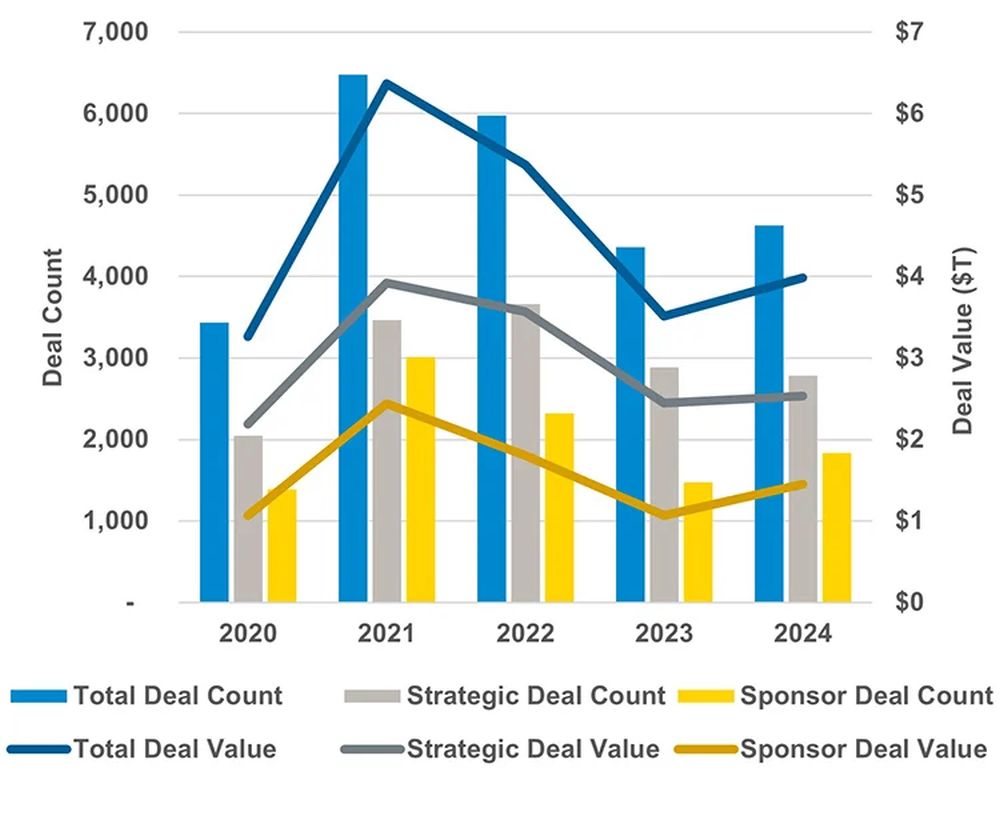

- M&A activity increased in 2024 by nearly all metrics as

dealmakers seized opportunities amid more favorable transacting

conditions, including consecutive interest rate cuts and tampered

inflation. - Aggregate value of transactions $100m+ increased significantly

in 2024 compared with 2023, up 14% across all buyer types.

Aggregate value of sponsor buyer deals led the increase with a 36%

jump, while strategic acquisitions held steady, up just 4%. - The number of transactions valued at $100 million or greater

increased 6% globally in 2024 vs 2023. Sponsor acquisitions jumped

24% by count, while acquisitions by strategic buyers held steady

(declining a marginal 3%). - The uptick in 2024 M&A activity was a noticeable rebound

following consecutive declines in dealmaking since 2021’s $6.4

trillion record.

4. Annual U.S. Crossborder Activity

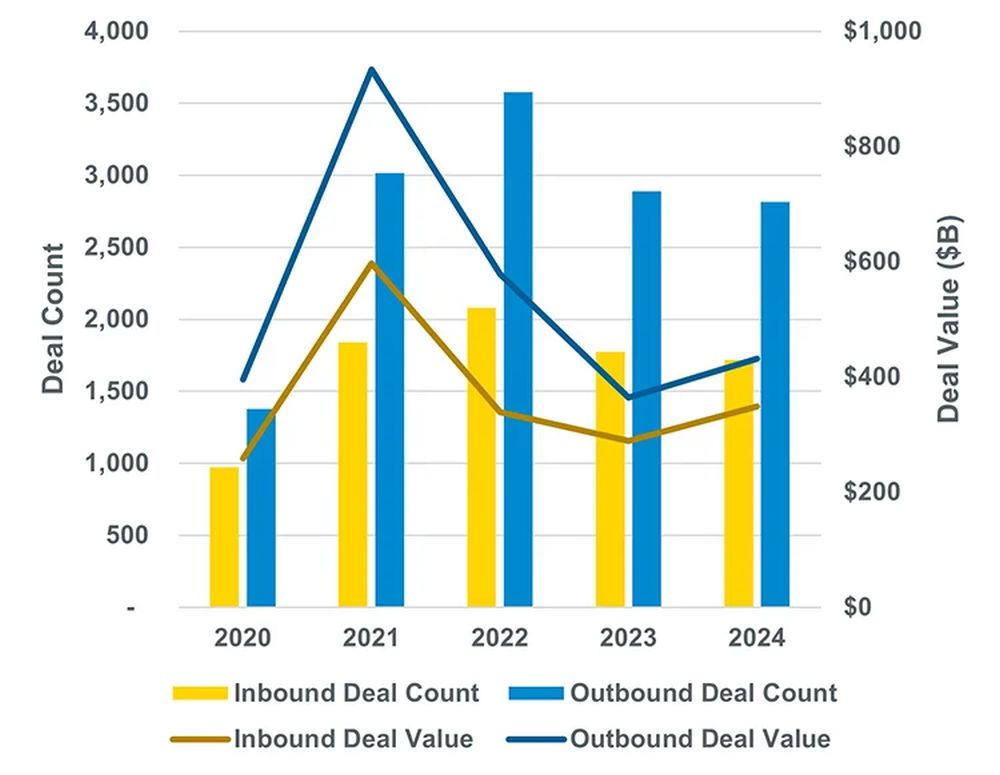

- Inbound U.S. activity in 2024 jumped 21% by deal value from

2023 and held steady by deal count (declining just 3%). The value

of U.S. companies acquired by non-U.S. buyers in 2024 totaled

nearly $350 billion. - Outbound activity in 2024 jumped 18% by deal value from 2023

and remained stable by deal count, declining just 3%. The value of

non-U.S. companies acquired by U.S. buyers in 2024 totaled over

$430 billion. - Canada-based acquirers drove the most inbound transactions in

2024 (287), followed closely by the UK (278). Japan-based buyers

took third at 147 transactions. - U.S. acquirers most frequently looked to targets in the UK

during 2024 (572), with Canada (382) and Germany (198) rounding out

the top three ex-U.S. target countries.

Active M&A Industries (U.S. Targets)

5. By Deal Count

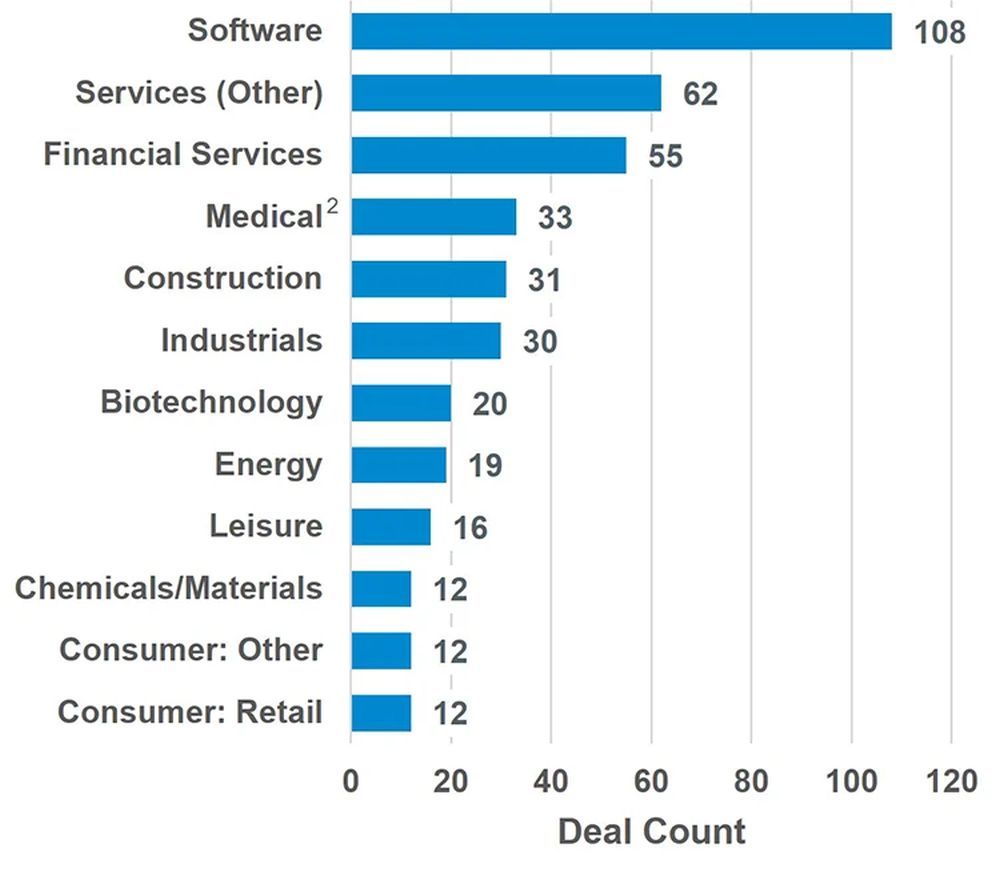

- The software industry once again topped the list of U.S.

M&A activity by deal count in December, continuing its streak

as the leading industry by volume and rounding out a full year at

number one. - Services industries also remained active, with financial

services and other professional services again rounding out the top

three sectors in December by deal count.

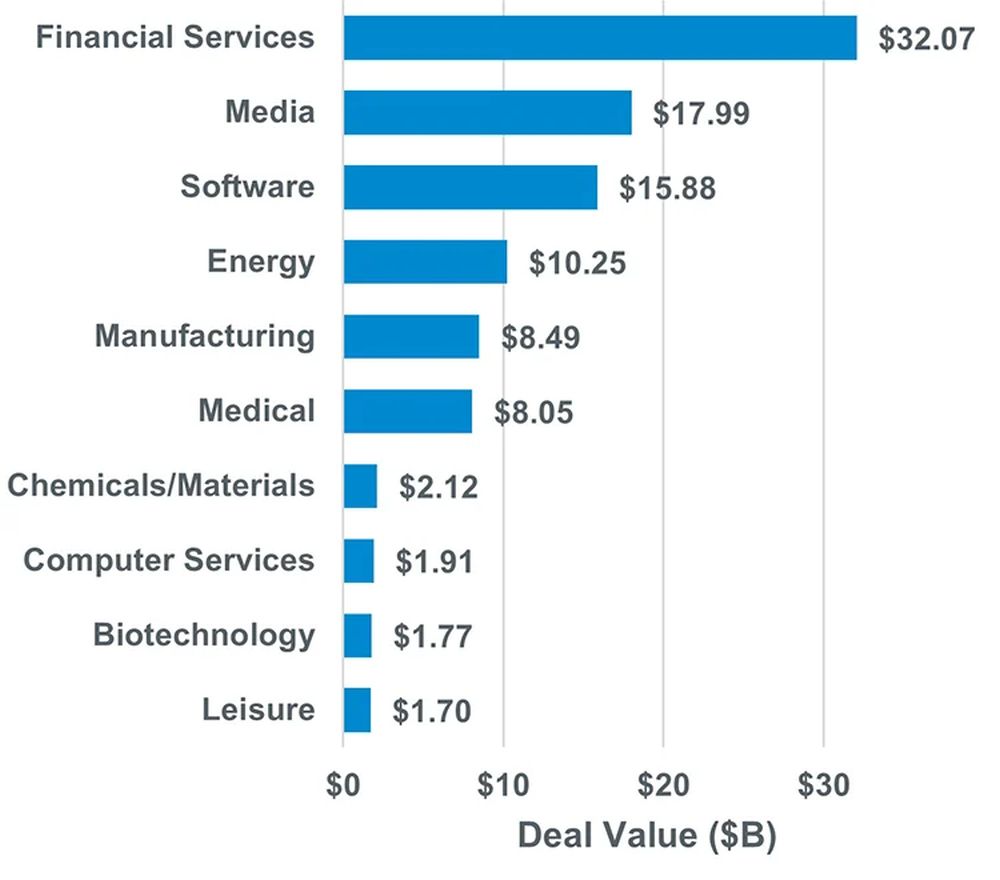

6. By Deal Value

- Financial services was the leading U.S. industry by deal value

in December, with two of the five largest deals of the month,

together totaling more than $25 billion in deal value. - Media was the second most active by deal value in December,

bolstered by Omnicom’s blockbuster acquisition of Interpublic.

Software targets were the third most active, at just over $15

billion in deal value.

December Blockbuster Deals

7. Largest U.S. Media Deal

Omnicom Group has agreed to acquire The

Interpublic Group of Companies, Inc. in an all-stock

transaction valued at approximately $13.75

billion.

8. Largest U.S. Asset Management Deal

BlackRock, Inc. has agreed to

acquire HPS Investment Partners, LLC in an

all-stock transaction valued at approximately $12

billion.

9. Selected Annual Highlights

More than 35 transactions exceeding $10 billion were announced

globally during the year, demonstrative of the comparably favorable

market conditions following tempered activity in 2023.

Transformative deals were struck in a variety of sectors, including

those highlighted below.

| Industry | Target | Buyer | Deal Value |

|---|---|---|---|

| Consumer Goods | Kellanova | Mars, Incorporated | $36 B |

| Financial Services | Discover Financial Services | Capital One Financial Corporation | $35 B |

| Software | ANSYS, Inc. | Synopsys, Inc. | $34 B |

| Media | Paramount Global | Skydance Media and RedBird Capital Partners | $28 B |

| Energy | Endeavor Energy Resources, L.P. |

Diamondback Energy, Inc. | $28 B |

| Pharma | Catalent, Inc. | Novo Holdings A/S | $16 B |

10 .2024 M&A Activity Recap

A snapshot of 2024 metrics, and how they stack up against

2023.

| 2024 | 2023 | Δ% | |

|---|---|---|---|

| Global Deal Value | $3.91 T | $3.49 T | 🡅 12% |

| Global Deal Count | 43,101 | 42,546 | 🡅 1% |

| U.S. Deal Value | $1.77 T | $1.58 T | 🡅 12% |

| U.S. Deal Count | 11,412 | 11,695 | 🡇 2% |

| # of $10B+ Deals (U.S.) | 27 | 22 | 🡅 23% |

Footnotes

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link