U.S. Cross-Border M&A: Mid-Year Outlook – Corporate and Company Law

The first two quarters of M&A

activity in 2025 have not achieved the banner-year levels that many

predicted; however, amid the uncertainty, there is still room for

optimism for a strong dealmaking environment to finish out the

year. We examine cross-border deal flows at the half-year mark to

provide insight into how tariffs and other trade developments

continue to shape the market sentiment—and the factors

hanging in the balance that could tip in favor of a more robust

deal environment for the remainder of 2025.

U.S. M&A deal environment

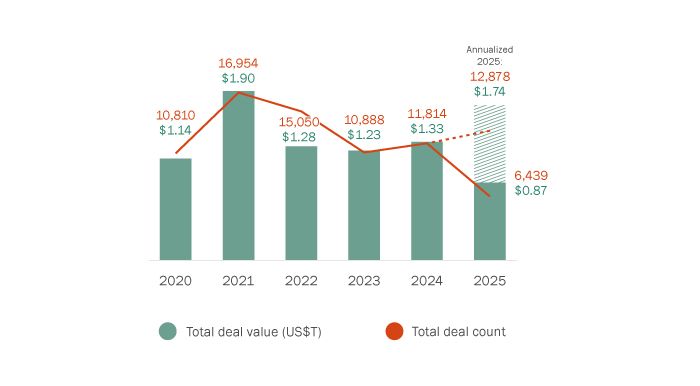

The picture of U.S. M&A deals remains mixed halfway into the

year, with combined global and domestic investment into U.S.

targets showing signs of a slowdown (see Figure 1), as ongoing

geopolitical volatility has had a chilling effect on dealmaking in

what was anticipated to be a comeback year for transactions. It

comes as no surprise that many dealmakers have opted for a

wait-and-see approach amid the flurry of U.S. tariff announcements

and the many subsequent pauses, adjustments and retaliatory

measures rolled out over the course of the last few months.

Dealmakers have also been impacted by stubbornly high U.S. interest

rates, as well as by uncertainty regarding the Trump

administration’s approach to antitrust enforcement.

That said, there are signs of life for deals involving U.S.

targets. U.S. domestic annualized deal value is projected to rise

moderately from $1.31 trillion in 2024 to $1.46 trillion in 2025

(see Figure 2), driven in part by high activity levels in

transactions exceeding $1 billion. This year is also currently on

track for a significant 29% YoY increase in deal value, though a

more moderate a 5% YoY increase in deal count for transactions

involving U.S. acquirers of U.S. targets (see Figure 2).

Figure 1: Deal value and count (any acquirer of U.S.

target)

Source: Bloomberg. Based on M&A deals announced during Jan

1, 2020 – June 30, 2025. Excludes terminated and withdrawn

deals.

Figure 2: Deal value and count (U.S. acquirer of U.S.

target)

Source: Bloomberg. Based on M&A deals announced during Jan

1, 2020 – June 30, 2025. Excludes terminated and withdrawn

deals.

Even as many deals remain paused, megadeals (with a value

greater than $1 billion) have sustained forward momentum. Whether

these megadeals represent a long tail of deals conceived in late

2024 or an optimistic indicator for 2025 remains to be seen. The

aggregate value of the 10 largest announced deals accounted for

around 34% of total deal value in the first half of 2025, with the

largest transaction valued at $39 billion (Sycamore Partners’

planned acquisition of Walgreens). Other notable announced

transactions include Charter Communications’ acquisition of Cox

Communications for $34.5 billion and Alphabet Inc.’s

acquisition of Wiz Inc. for $32 billion.

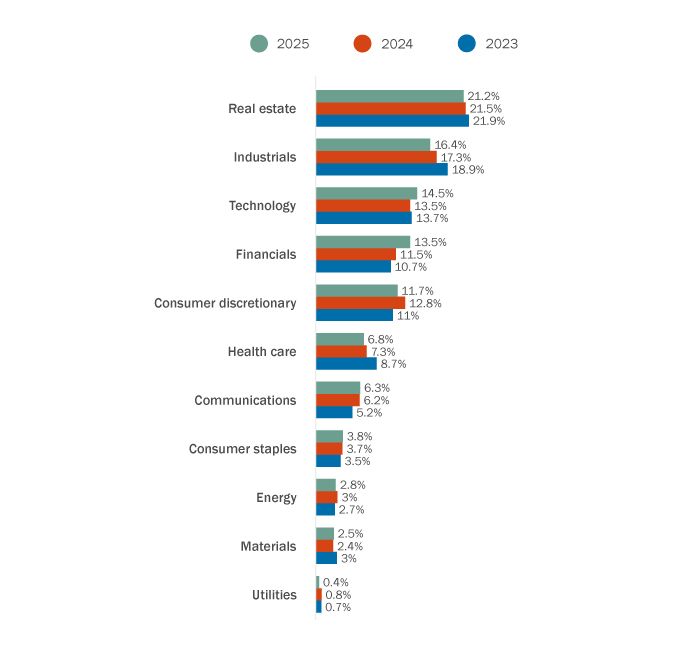

In terms of sector-focus, U.S. acquirers are finding

opportunities in real estate, which is the top sector by deal count

YTD (see Figure 3). New alternative real estate asset classes have

increased M&A activity in recent years1, while more

traditional real estate assets (e.g., housing and offices) remain

tied, in part, to the outcome of interest rates and the knock-on

effects from tariffs on construction costs, supply and valuations.

However, real estate’s intersection with digital infrastructure

(e.g., data centers, cables and energy-generating facilities) has

helped fuel some of 2024’s megadeals, including the $16 billion

acquisition of AirTrunk by Blackstone2, and show signs

of sustained growth for 2025. Technology also continues to be a

bright spot as investors remain engaged in cloud computing,

AI-enhanced software and cybersecurity, among other assets in the

tech sector tied to the AI boom. The market expectations for this

sector remain high and will likely continue to be a focus of

investment for the remainder of the year, as exemplified by

xAI’s acquisition of X Corp. for $33 billion in March.

Figure 3: Target industry breakdown (U.S. acquirer of

U.S. target)

Source: Bloomberg. Based on M&A deals announced during Jan

1, 2020 – June 30, 2025. Excludes terminated and withdrawn

deals.

Global deal flows

Investment from Canada into the U.S.

U.S. inbound investment from Canada seems unlikely to return to

high-water marks of 2021 and 2022; however, based on the projected

annualized deal value of $62 billion, it appears that 2025 may

prove to be a modest improvement over last year’s weak

performance. The continued slowdown of Canadian investment to the

U.S. from 2023 and 2024 is emblematic of the larger themes of

uncertainty in global trade relations as well as the particular

uncertainties in U.S.-Canada trade relations. On the other hand,

the promise of a potential U.S.-Canada trade deal (following the

rescission of Canada’s planned digital services tax) could

alleviate uncertainty for Canadian investors in the U.S. and

encourage M&A activity.

While deal volume remains low in most sectors after years of

high inflation and financing challenges, we continue to see

Canadian acquirers look to the U.S. for opportunities, with a

moderate uptick in the proportion of deals valued over $1 billion

and those valued between $100 million and $500 million compared to

last year. In particular, Canadian acquirers in the financial

sector have accounted for the greatest proportion of U.S.-inbound

deals announced YTD, which are up 8% this year compared to the

proportion of deals announced in 2024 (see Figure 5). The share of

deals from energy acquirers has also seen a modest increase (3%

over 2024), which may reflect a renewed focus on energy security

acquisitions, such as Keyera Corp.’s deal to buy the Canadian

natural gas liquids business of the U.S. firm Plains, announced in

June3. Conversely, the share of deals by Canadian

acquirers in the materials sector is down 5% from last year, likely

due to the sector’s vulnerability to the whipsawing of U.S.

tariffs and retaliatory measures worldwide. Even before the most

recent announcement of 35% tariffs on Canadian goods, U.S. tariff

rates in 2025 have been at their highest levels since

19394, continuing to burden businesses with

international supply chains.

Figure 4: Deal value and count (Canadian acquirers of

U.S. target)

Source: Bloomberg. Based on M&A deals announced during Jan

1, 2020 – June 30, 2025. Excludes terminated and withdrawn

deals.

Figure 5: Acquirer industry breakdown (Canadian

acquirers of U.S. targets)

Source: Bloomberg. Based on M&A deals announced during Jan

1, 2020 – June 30, 2025. Excludes terminated and withdrawn

deals.

Investment from the U.S. into Canada

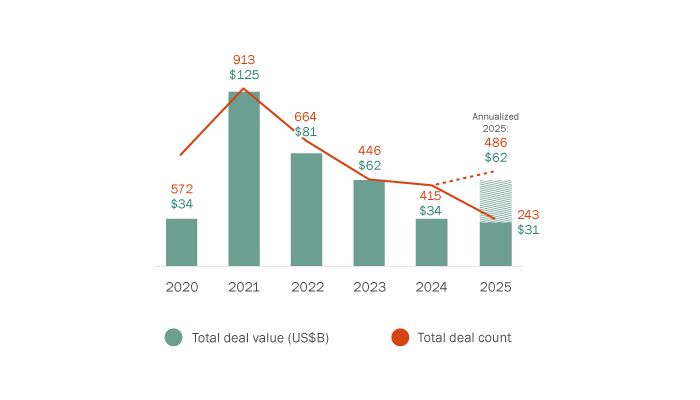

The current geopolitical environment is having a significant

impact on deals into Canada. Deal activity from the U.S. into

Canada appears to be softening following a stronger year in 2024,

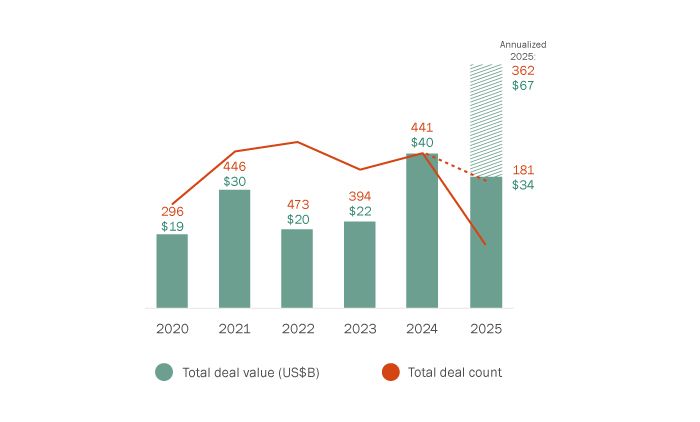

with annualized deal count projected to reach 362 deals, down from

last year’s 441 deals (see Figure 6). Adding to the chilling

effect, the Canadian government updated its Guidelines on the National Security Review of

Investments to consider, when reviewing foreign investment into

Canada, the potential of the investment to undermine Canada’s

economic security through the enhanced integration of the Canadian

business with the economy of a foreign state.

That said, deal value is expected to outpace last year at a

projected $67 billion (compared to $40 billion in 2024). This

points to a shift from last year for U.S. buyers of Canadian

assets, who are focusing on larger M&A deals. For example,

Sunoco’s planned $9 billion acquisition of Parkland Corp is the

largest announced deal involving a U.S. acquirer and a Canadian

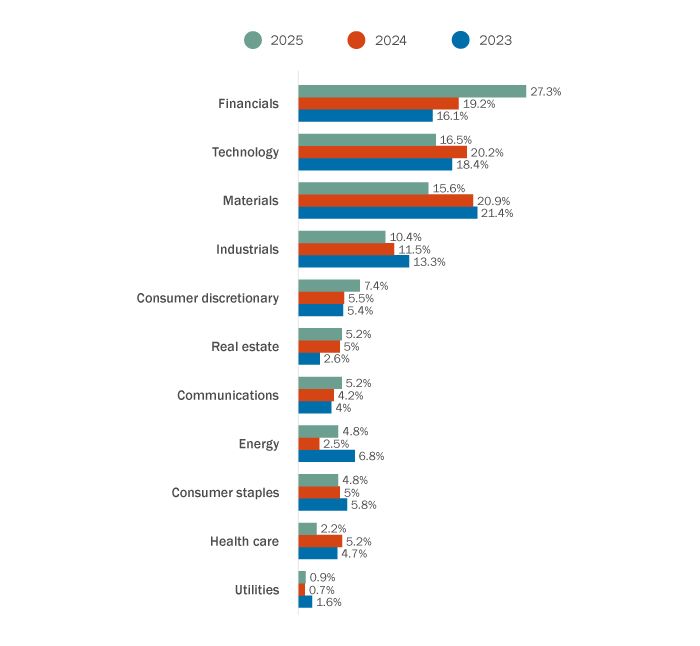

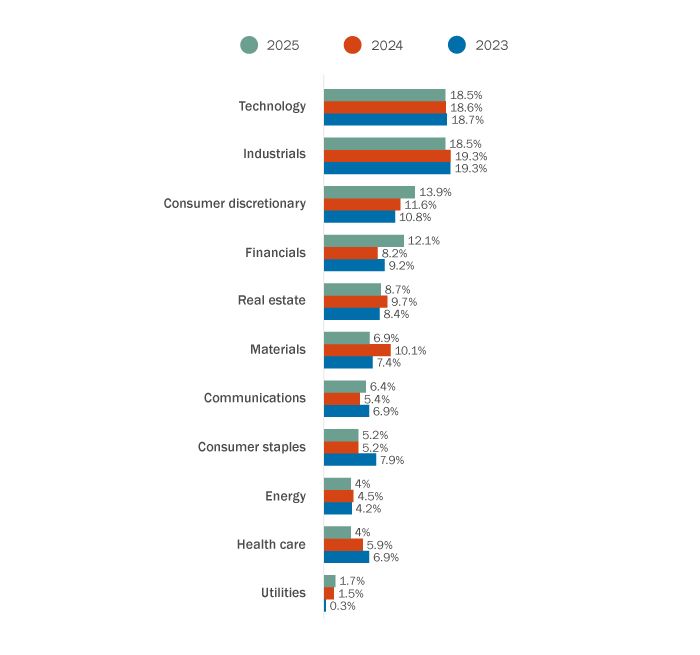

target since 2020. Transactions in the financial sector have grown

significantly (see Figure 7), likely bolstered by steadying

inflation rates as the Bank of Canada maintains its target interest

rate at 2.75%5. Industrials are down somewhat but retain

their status over the last three years as a top target industry.

Notwithstanding tariff risk, industrials’ strong earnings and

tailwinds from infrastructure activity suggest that this sector

will continue to remain of interest for U.S. acquirers.

Figure 6: Deal value and count (U.S. acquirer of

Canadian target)

Source: Bloomberg. Based on M&A deals announced during Jan

1, 2020 – June 30, 2025. Excludes terminated and withdrawn

deals.

Figure 7: Industry breakdown (U.S. acquirer of Canadian

target)

Source: Bloomberg. Based on M&A deals announced during Jan

1, 2020 – June 30, 2025. Excludes terminated and withdrawn

deals.

Spotlight on Japan

Japan has gained significant traction on the global M&A

stage in the last several years. Market reforms and shareholder

activism aimed at increasing shareholder value have led to

increased Japanese investment into North America. Annualized deal

value for Japanese acquirers of U.S. and Canadian targets is up so

far in 2025 (by 43% for Canadian targets in

particular)6. Canada’s consumer discretionary,

materials and consumer staples are the top target for Japanese

investors, with a focus on smaller transactions (less than $100

million). Investment from Japan into Canada is further supported by

the two countries’ collaboration on the Comprehensive and

Progressive Agreement for Trans-Pacific Partnership, which

eliminates or reduces tariffs on most key Canadian exports to

Japan, including for agriculture, seafood, forestry, and metals and

mineral products7.

Conclusion

While 2025 has so far not met market expectations, there have

been improvements over 2024 and dealmaking may rebound further

depending on how several issues play out, including tariff

policies, inflation rates and overall market sentiment. Buyers and

sellers may adjust their playbooks once again as countries,

including Canada, continue to negotiate trade deals with the United

States8. If tariff and trade tensions settle, investors

may be able to more precisely make the assessments they need to get

deals over the finish line, with the possibility of increased

activity towards the year’s end.

Footnotes

1. See PwC, “Global M&A Trends in Real Estate”,

(June 24, 2025).

2. See Blackstone, “Blackstone Announces Agreement to Acquire AirTrunk

in a A$24B Transaction”, (September 4, 2024).

3. See BNN Bloomberg, “Keyera says $5.15 billion deal to buy Plains’

Canadian business to help energy security”, (June 17,

2025).

4. See EY, “US economic outlook May 2025”, (June 20,

2025).

5. Bank of Canada, “Policy interest rate”, (June 4,

2025).

6. Source: Bloomberg. Based on M&A deals announced

during Jan 1, 2020 – June 30, 2025. Excludes terminated and

withdrawn deals.

7. See Government of Canada, “Canada-Japan relations”, (June 7,

2025).

8. The Financial Post, “Where does Canada stand as Trump’s tariff

deadlines loom”, (July 8, 2025).

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link