U.S. Private Equity Market Recap – January 2025 – Corporate and Company Law

RG

Ropes & Gray LLP

Ropes & Gray is a preeminent global law firm with approximately 1,400 lawyers and legal professionals serving clients in major centers of business, finance, technology and government. The firm has offices in New York, Washington, D.C., Boston, Chicago, San Francisco, Silicon Valley, London, Hong Kong, Shanghai, Tokyo and Seoul.

Read our latest insights into the U.S. private equity market. We cover monthly deal activity and size, fundraising, exits, leveraged loans, and a look ahead.

United States

Corporate/Commercial Law

To print this article, all you need is to be registered or login on Mondaq.com.

Read our latest insights into the U.S. private equity market. We

cover monthly deal activity and size, fundraising, exits, leveraged

loans, and a look ahead. To receive our private equity thought

leadership, please join our mailing list.

Key Takeaways

- U.S. PE deal activity:Deal activity was

slightly down in 2024 with a 3% YoY decline, while deal value was

up 14%. Transaction activity did not make the strong comeback

dealmakers were hoping for in 2024 as investors navigated market

uncertainty around rate cuts and the 2024 presidential

election. - Difficult fundraising

environment: U.S. PE fundraising was down

in 2024 on both a fund-count and capital-raised basis. The 2024

fundraising market was particularly difficult for smaller firms and

first-time managers. - Positive 2025 outlook:

Dealmakers are optimistic that M&A will pick up this year as

various market forces are expected to boost deal activity. A Teneo

survey showed that 83% of CEOs and 87% of investors are expecting

more M&A activity in 2025.

2024 Recap

- Macroeconomic backdrop held strong: The

recession risk heading into 2024 did not materialize and a new

cycle of rate cuts began. The Fed made its first long-awaited rate

cut in September and cumulatively cut rates by 100 bps by year

end. - U.S. presidential election concludes:

Trump’s election win resolved market uncertainty around the

next administration. - Lackluster dealmaking comeback: Private equity

deal activity didn’t make the robust comeback that industry

participants were hoping for in 2024. - Trends in deal activity: 2024 experienced an

uptick in large take-private deals, an increase in corporate

carve-outs, and a trend toward larger deal sizes. - Rebound in exit activity: PE exits began to

ramp up in 2024 but remain below normalized levels. Pressure to

return LP capital persisted throughout the year and sponsors used

an array of strategies, such as minority sales and continuation

funds, to unlock liquidity. - Major drop in fundraising: Both the number of

funds closed and amount of capital raised fell for U.S. PE funds in

in 2024 as capital gridlock persisted in the industry. - Challenging environment for emerging managers:

First-time managers and smaller firms struggled as LPs showed a

preference for experienced managers, resulting in capital largely

concentrated among larger managers and funds. - IPO market improved: The U.S. IPO market began

to unthaw in 2024 amid a buoyant equity market, but PE-backed

companies mostly remained on the sidelines.

Improved investor sentiment: The cautious optimism that started

the year gave way to a rise in investor confidence by the end of

2024.

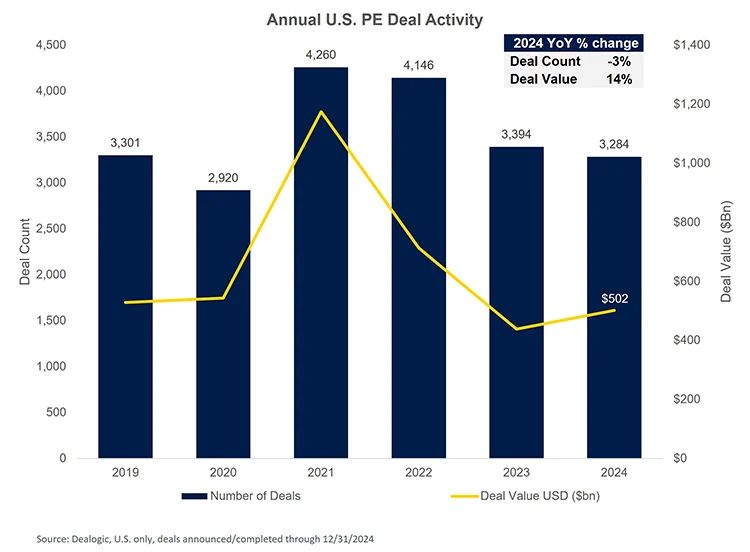

U.S. PE Deal Activity

- Activity remained suppressed: 2024 annual deal

count was down compared to 2023. While deal value increased YoY, it

finished below historical levels. - 2024 deal markets in limbo: Investors spent

much of 2024 waiting for clarity on monetary policy and potential

rate cuts, macro conditions to continue improving, and more

conclusive policy outlooks following the presidential

election. - Optimistic outlook: Investor sentiment is high

heading into the new year and dealmakers are expecting deal

activity to pick up in 2025. - Factors to drive 2025 deal activity: In

addition to increased CEO and investor confidence, high levels of

dry powder, an incoming pro-business and growth Trump

administration, and pressure to exit and return LP capital are

expected to boost transaction activity.

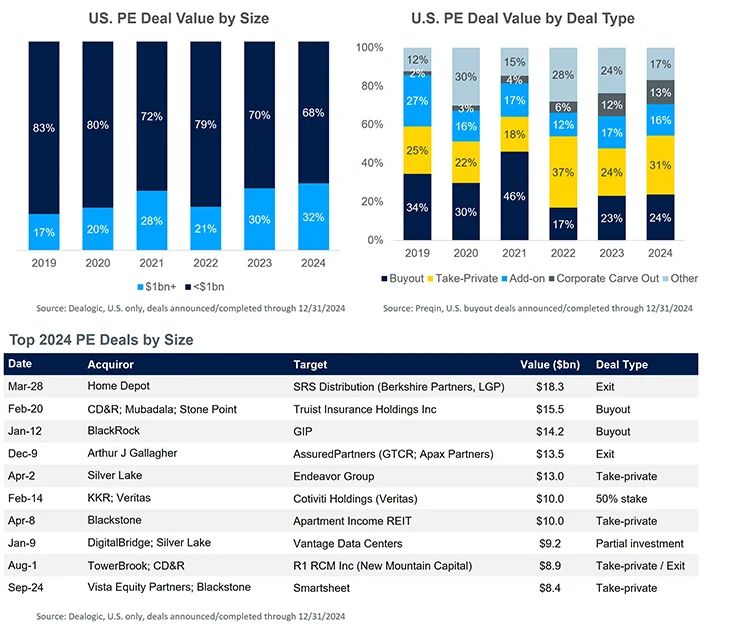

Trends in U.S. PE Deals: Size and Type

- Deal size increasing: The proportion of deals

over $1 billion increased in 2024 and the average PE deal size

increased in 2024 after falling for two consecutive years. - 2024 deal type trends: Take-private deals grew

in popularity as PE firms had high levels of dry powder and jumped

on opportunities to acquire companies they deemed undervalued by

public markets. Another deal type favored by PE firms in 2024 was

corporate carve-outs, a trend expected to continue into 2025.

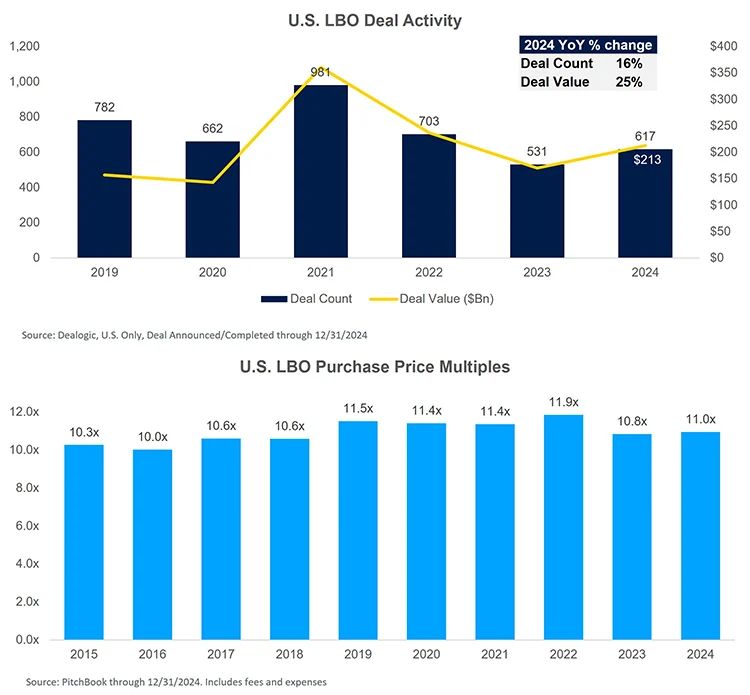

Trends in U.S. PE Deals: LBOs

- LBOs pick up: U.S. LBO deal counts and value

picked up in 2024 after two consecutive years of decreasing

activity. Interest rate cuts and strong financing markets helped to

fuel leveraged buyout activity. - Purchase price multiples up: Average LBO deal

multiples for 2024 finished at 11.0x. Valuation gaps between buyers

and sellers are continuing to close as financing becomes less

expensive and market conditions normalize.

Trends in U.S. PE Deals: Exits

- Exits start to rebound: The number of PE exits

picked up in 2024, but the value of exits remained below historical

levels. - Maturity wall builds: The maturity wall facing

PE firms globally will continue to grow in the coming years as GPs

look to wind down older vintages that are entering their harvesting

age. Firms will face pressure to ramp up exit activity to realize

gains on investments and return LP capital.

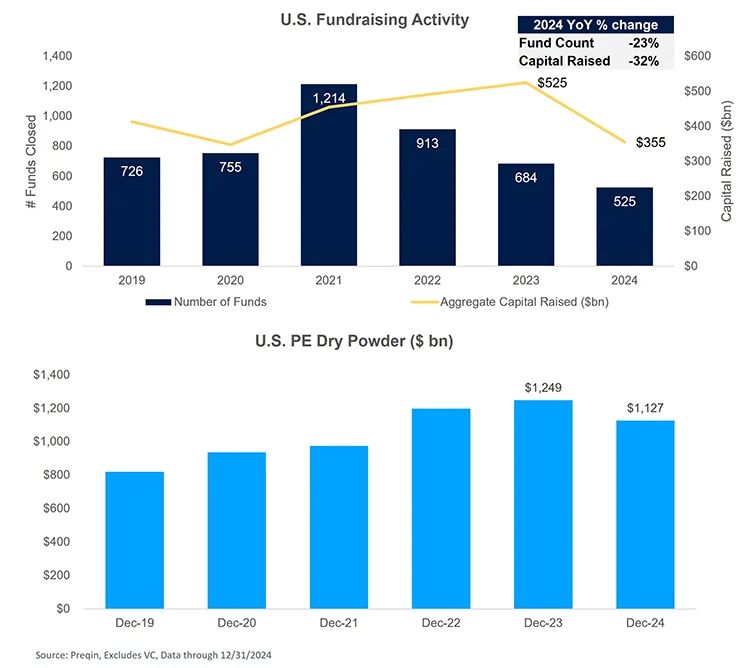

U.S. Fundraising & Dry Powder

- Fundraising drops: Both the amount of capital

raised and number of funds closed fell in 2024 as the fundraising

environment continued to face challenges. - Dry powder ticks down: Despite dropping by

~10% in 2024, U.S. PE dry powder remains elevated at over $1.1

trillion. Investors continue to face pressure to put raised capital

to work, which dealmakers are predicting will help spur transaction

activity in 2025.

U.S. Fundraising Trends: Size and Experience

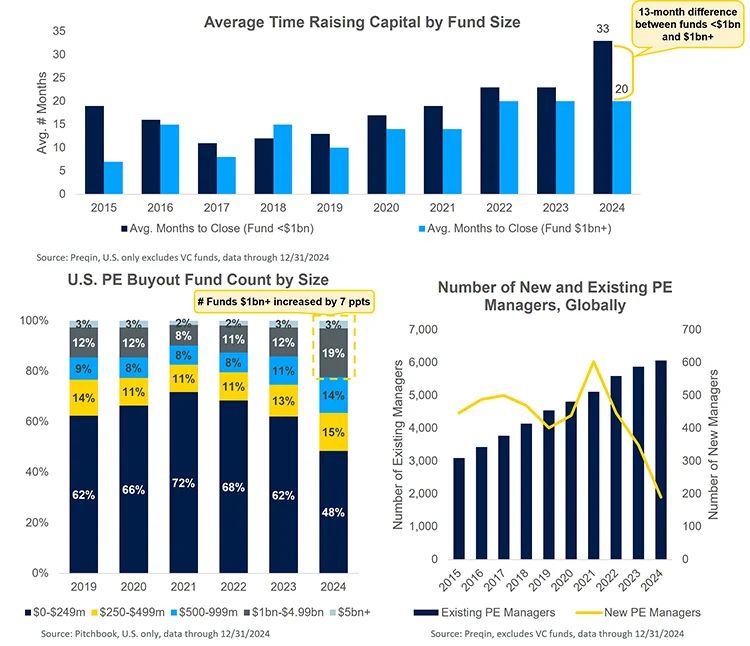

- Longer fundraising cycle: The average length

of fundraising jumped from 21 months in 2023 to 27 months in 2024

for all U.S. PE funds. However, funds over $1 billion had an easier

time raising capital, taking only 22 months on average to close,

while funds under $1 billion took 33 months. - Investors prefer larger funds: U.S. PE funds

over $1 billion attracted 22% of raised capital in 2024, up from

15% of capital raised in 2023. - New managers plummet: As the fundraising

market is particularly challenging for new firms, the number of new

PE managers has dropped dramatically.

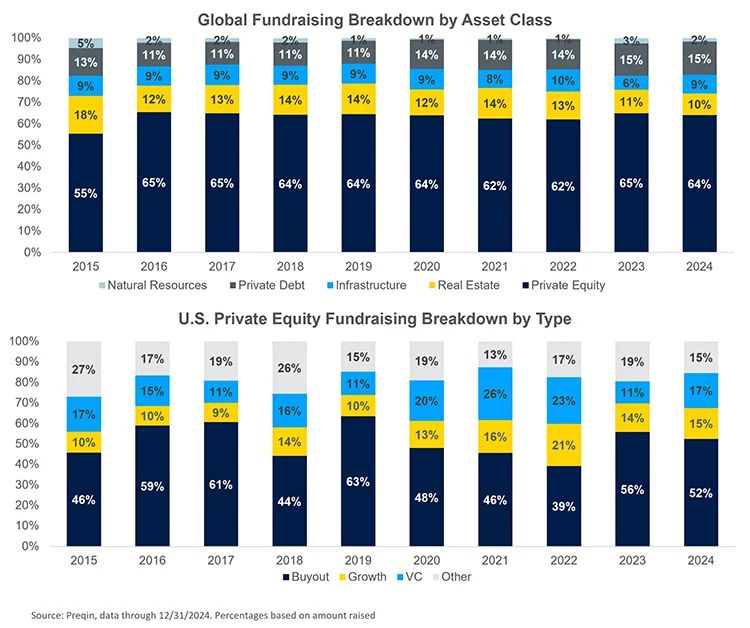

U.S. Fundraising Trends: Asset Class

- Private debt stays hot: Private credit

remained a hot sector within alternatives in 2024. Large managers

are continuing to grow as the industry is experiencing

consolidation following a wave of M&A deals. - Infrastructure grows: Infrastructure continues

to attract capital as investors eye opportunities within the

sector, particularly those related to digital infrastructure. - Growth and VC gain: Growth and VC strategies

raised a higher proportion of total U.S. PE capital raised in 2024,

compared to 2023. Growth strategies specifically have been higher

than pre-pandemic levels over the last 3 years.

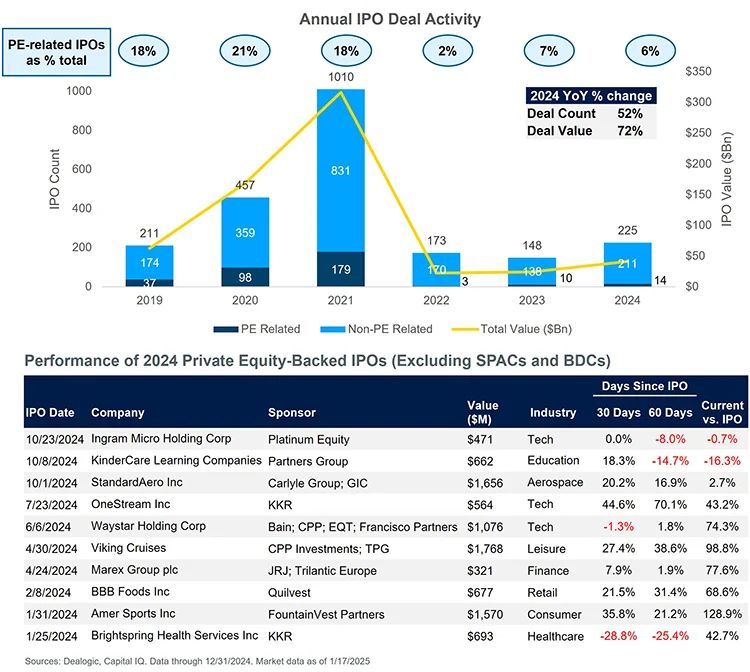

IPO Activity

- U.S. IPOs pick up: Amid a strong year in U.S.

public equities markets, the U.S. IPO market started to recover and

ended the year with an increase in deal activity from 2023. - PE-backed IPOs remain sidelined: PE-backed

companies were mostly on the sidelines while the U.S. IPO market

started to recover in 2024. However, industry analysts expect PE

firms will be more active in the IPO market in 2025.

Trump’s Second Term: Potential Implications

Investors’ views

- Investors had a positive reaction following the election and

believe Trump’s pro-growth and pro-business leanings will help

drive M&A activity. - However, industry players also caution that some of Trump’s

anticipated policies may create headwinds and to expect volatility

as the market navigates various policy implications. - Investors will look to Trump’s first 100 days in office to

provide an indication of how different policies such as trade,

immigration, energy and tax will all come together to affect the

business and investing landscape.

Key policy areas to watch

| Regulatory | “America-First” | Economic |

|---|---|---|

|

|

|

Industry-specific impacts

2025 Outlook

- Slower pace of rate cuts: The Fed has

indicated that the pace of rate cuts will slow in the months ahead.

Investors are anticipating anywhere between zero and four rate cuts

throughout the year and do not expect rates to get under 3% by the

end of 2025. - Positive outlook for dealmaking and exits:

Dealmakers are optimistic heading into 2025 and expect significant

upside for PE activity in the year ahead. As a growing proportion

of assets reach their harvesting period, firms will face mounting

pressures to exit.

| Dynamics expected to drive transaction

activity |

|

|---|---|

| ✔ Rate cuts helping to lower cost of capital | ✔ High levels of dry powder |

| ✔ Stabilizing market environment and ‘Trump

Bump’ |

✔ Pressure to exit and return LP capital |

- Mid-market opportunities: Industry analysts

expect investors to continue pursuing opportunities in the mid

market in 2025 and anticipate these strategies will continue to

perform strongly. Mid-market investments offer scalability and

strike a balance between utilizing leverage and improving

operational efficiencies to create value and drive returns. - Mixed fundraising outlook: PE firms are

optimistic the fundraising environment will improve as exits pick

up and more capital is returned to LPs. However, capital raised is

not projected to meaningfully increase in 2025, primarily due to

fewer mega funds expected to close in the year. - PE-backed IPOs poised for comeback: The IPO

landscape is expected to shift in 2025, especially for PE-backed

companies. Bankers and analysts are gearing up for a revival in the

IPO market and expecting a flurry of listing announcements in the

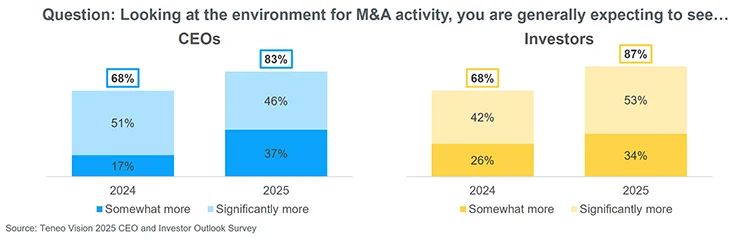

first half of 2025. - 2025 M&A expectations: Both CEOs and

investors have more favorable outlooks for M&A in 2025 compared

to expectations going into 2024.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link