What’s Next For EU Sustainability Policy? – Corporate and Company Law

GT

Grant Thornton Malta

We combine global scale with local insight, quality and understanding to give you the assurance, tax, and advisory services you need to realise your ambitions.

In a surprising move on 22 October 2025, the European Parliament rejected the mandate for the proposed Omnibus Regulation, creating a pause in the EU’s sustainability reform agenda.

European Union

Corporate/Commercial Law

To print this article, all you need is to be registered or login on Mondaq.com.

Grant Thornton Malta are most popular:

- within Employment and HR, Immigration and Privacy topic(s)

- in European Union

- with readers working within the Banking & Credit industries

In a surprising move on 22 October 2025, the European Parliament

rejected the mandate for the proposed Omnibus Regulation, creating

a pause in the EU’s sustainability reform agenda. The proposal

will now return to the plenary session on 11–13 November,

where Members of Parliament will debate and vote on the package in

full and possibly reopen parts of it for amendment. The rejection

highlights growing political tensions around the future of EU

sustainability legislation and raises critical questions about the

direction of the European Green Deal.

What happened at the vote?

Parliament voted against giving the green light to move the

Omnibus compromise forward, meaning the proposal will undergo

another round of discussion in November. This decision has added a

layer of uncertainty to the legislative process. Instead of being

fast-tracked, it now heads back to plenary, where it will be

debated and voted on in full. A new deadline for amendments will be

set, which means parts of the compromise could be reopened,

potentially reshaping the proposal. This also risks delaying

progress and unravelling agreements that had already been

reached.

What is the Omnibus Regulation?

Introduced by the European Commission on 26 February 2025, the

Omnibus package is a simplification initiative aimed at easing

compliance with the EU’s sustainability framework.

It proposes amendments to three cornerstone laws of the European

Green Deal:

The main objective is to reduce reporting burdens, particularly

for mid-sized companies, while maintaining consistency and

competitiveness in the EU’s sustainability agenda.

Key changes proposed

1. CSRD

The Omnibus proposes a narrower scope for CSRD, limiting

mandatory reporting to companies with:

As a result…

2. EU TAXONOMY

- Reduced scope aligned with CSRD thresholds.

- Gradual adoption through partial alignment.

- Materiality thresholds (e.g., 10% of turnover or assets).

- Simplified DNSH criteria and fewer reporting templates.

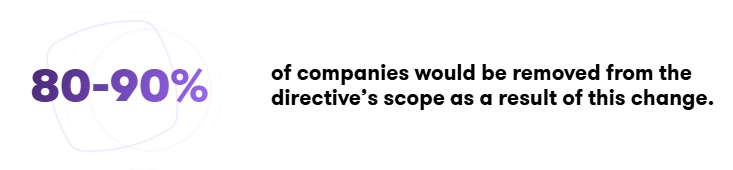

2. CSDDD

The directive’s scope is significantly reduced to companies

with:

These proposals were intended to shift the focus from the

quantity of reporting to its quality and proportionality — an

aim that will now be reconsidered as Parliament revisits the file

in November.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link